401k Loans 101

June 28, 2011

If you’ve been setting investing goals and decided your 401k was a good place to invest your money then you probably have some money built up in your retirement account. What if you discover you need that money you’ve been putting aside before retirement?

You may be able to take a 401k loan, where you can borrow against the money you’ve accumulated in your retirement account. If you find yourself in a tough situation where you need money quickly a 401k loan might be tempting but be aware there are some potential risks. Today we’ll look at the pros and cons of a 401k loan and some frequently asked questions.

401k Loan Rules

How does a 401k loan work? Your best resource is your plan sponsor. Each employer-sponsored plan can be different, and your plan is not required to allow you to take a loan.

If your plan does allow you to borrow from your 401k plan, these rules apply:

- you may only borrow a maximum of 50% of your vested account balance, with a cap of $50,000

- unless you are buying a home, you must repay the loan within 5 years of borrowing the funds

- you must make consistent payments (at minimum, one per quarter) until the debt is repaid

Upside to borrowing From Your 401k

It seems like a pretty good deal. You can borrow from yourself, and the interest you pay back on the loan goes back into your retirement pocket. You don’t end up losing money by paying interest to a bank or credit card. The interest you pay goes from your checking account to your retirement account. It stays under your control. That is a major benefit of borrowing from your 401k plan.

A second benefit is no credit check is required. There are no qualifications set in place. You don’t have to have a certain credit score: the money is yours to borrow as needed.

Risks of Taking a 401k Loan

As nice as paying yourself interest sounds, there are some significant risks to consider with this type of borrowing. The first major concern is that any change in your job status normally means you must repay the loan within 60 days. That means if you lose your job or willingly leave the company, you must have funds available to repay the loan almost immediately. If you’ve just lost your job it might be difficult to repay the loan that fast.

If you can’t repay the loan, whether through job loss or not, your initial withdrawal of the funds will be treated as a taxable distribution. You will then owe income tax on the funds you borrowed plus a 10% fee to the IRS assuming you are under age 59 and a half. Even if you can eventually repay the loan, you will pay an origination fee and potentially a maintenance fee tacked on top of it. Your “free loan” to yourself probably won’t be exactly free.

Another risk is the potential loss of investment gain from removing funds from your portfolio. It would be great to avoid a market crash if you could time the market (something that is impossible to really do), but what if your portfolio grows 50% over that maximum 5 year loan period? The investment gains you leave behind can make other forms of borrowing look inexpensive in comparison.

An additional consideration is borrowing when times get tough sets up a bad habit of borrowing. When your expenses go up, your income goes down, or both, the last resort is to borrow money. A better course of action is to cut back on your expenses or find a way to increase your income again. Borrowing from your 401k is a risky, but easy “out” in this situation.

Alternatives to Borrowing From Your Retirement Plan

As mentioned above the best alternative to borrowing from your financial future is to cut back, sell items you own, or grow your income. Borrowing shouldn’t be your first option.

You could consider taking a home equity loan or utilizing a home equity line of credit, but in doing so you will be paying interest to the lender rather than to yourself. The upside to a HELOC over a 401k loan is the loan does not instantly become due if you change or lose your job.

In recent years a new credit market has emerged that offers person-to-person loans. There are a few P2P lending companies like Lending Club and Prosper that let you apply for loans that are funded by a group of other people. You still have to go through a loan application process and they evaluate your credit but the fees and rates can be less than going through a bank.

If you need money for a short period of time and don’t mind increasing your risk, you may be able to swing a 0% financing deal with a new credit card. Of course the credit card company is willing to take this risk on the assumption that you will slip up at some point in the future, and owe them a lot in fees and interest charges.

401k Loan Frequently Asked Questions

Q: How much can I borrow from my 401k?

A: Up to 50% of your total vested account balance to a maximum of $50,000. You could borrow $50,000 only if your account had at least $100,000 in it.

Q: Is borrowing from my 401k tax deductible?

A: No.

Q: How quickly do I have to repay the loan?

A: Within 5 years of borrowing unless you leave the company or lose your job. Your 401k loan cannot be rolled over to a new plan, and your loan may be due within 60 days of a job status change. (If you borrow to finance a home purchase, your terms can be longer — up to 15 years.)

Q: What fees will I incur with a 401k loan?

A: You will owe yourself interest, and pay an origination fee to the plan sponsor. You may also pay a maintenance fee. If you cannot repay the loan it will be treated as a non-qualified distribution and you will owe the IRS a 10% fee plus income tax on the amount borrowed.

College Graduate Roundup

May 22, 2011

Graduation parties can be a bittersweet event for college graduates. You’re relieved that all your hard work has paid off and you finally have your degree. It’s definitely a good reason to have a big party but as you celebrate with your classmates you realize that life as you know it is ending. While the new chapter in your life will be exciting, you’ll miss your friends and the lifestyle of being a student, and you’re also a little worried about post-college life.

Life After College

I went to my cousin’s graduation party last weekend and she already had a jump on “life after college”. She has a job and an apartment lined up and like many college graduates will start making more money than she’s ever earned in her life. Not only that, she won’t have to spend every evening studying her brains out, she can come home from work and the night will be hers.

Spending Money

The bad news is that with all this free time and a new paycheck you’ll find ways to start spending your money. To start with, if you borrowed money you’ll have to start paying off student loans that you accumulated on your quest for wisdom.

Once you get a job and are no longer your parent’s dependent you’ll also have to look into post graduate health insurance plans and figure out the best balance of insurance premiums and deductibles for your medical needs. One tip, if you do have any major medical procedures that you know you’ll need it’s good to try and get them done while you’re still on your parents insurance.

Saving Money

If you’re starting to get a paycheck you might feel flush with cash since you’re used to the student sized bank account. You definitely want to put together a savings plan to cover your bills and avoid blowing all your newly earned money. This is even more important if you haven’t found a job in your field yet and don’t have much of income to support those expenses.

When you’re a recent college grad the expenses like insurance, groceries, gas, and rent can pile up faster than you realize. You’ll want to try and cut your costs with things like finding an affordable apartment and looking for ways to save on auto insurance.

Money for the Future

Although you’re just getting your financial feet under you, it’s not to early to start thinking about your financial situation a decade or more in the future. If you want to buy a house someday, check out this post on credit scores for college graduates.

Your credit score is becoming more and more important in your financial life and you’ll want to start building your credit history. One way to kickstart your credit history is with a secured loan or a secured credit card. If you already have some credit established and think you’d qualify for a credit card then a rewards card is an option. Don’t open one if you’d carry a balance but if you pay it off every month a card can help your credit – here’s a look at some of the best credit cards for college graduates.

Something else to consider is to start investing money, whether it’s in a regular investment account or a retirement plan like a 401k or IRA – here are some investing tips for college grads.

Understanding Finances

Our public schools and even universities in the U.S. don’t do the best job about educating you on personal finances and how to handle your money. One of the best investments of your time when you finish school is to spend an hour each week reading up on some aspect of your finances. Below are some articles from blogs that I recommend subscribing to. All of these sites publish several articles a week across a variety of personal finance topics. Of course magazines and books are also great resources and many of these blogs have a preferred reading list you can check out.

Congratulations on graduating!

Personal Finance

- Creating a Budget: Money Management 101

- Finance and Techology Innovation Comes to Life

- Your Money Values: How Do You Value Your Money vs Time?

- 8 New Financial Words Added to the Dictionary Since the Recession

- Why Routine Living Can Leak Your Money

- How to Zig When Others Zag: The Contrarian Approach to Personal Finances

- What’s the Best Financial Advice You’ve Ever Received?

- Carnival of Personal Finance

Investing

- Use Oil Stocks As A Hedge Against Rising Gas Prices

- Stock Chart Reversal Patterns – Head and Shoulders

- Reasons Not to Buy Stocks

- Can the US Government Seize Your 401k or IRA?

- Investing versus Gambling in the Stock Market

- Index Investors Can Be Aggressive Too

3 Ways to Buy More House for Less Money

April 25, 2011

When you buy a house, you are making a major purchase, probably one of the largest in your lifetime. Although buying a home will never be “cheap,” there are ways that you can get a little more for less.

Why does it seem like the place you want most when house hunting is often the one at the top of your budget? Only you can determine how much house you can afford. However, if you’re getting frustrated and having trouble finding homes that meet all your criteria and are in your price range, here are a few tips that can help lower the price of your home.

First we’ll look at lowering the cost of borrowing money to pay for your home. Then we’ll move on to finding the square footage and features you want at a price you can better afford.

1) Lower Your Credit Score & Interest Rate

One of the best things you can do is work to improve your credit so that you get a better interest rate. The interest that you pay on a home purchase can make a big difference in how much you pay over the life of the loan. Indeed, you could pay tens of thousands of dollars more over the life of your mortgage just by having to pay an interest that is 1% higher.

The reason it makes such a big difference is because you’re often borrowing large amounts of money and then paying it off over 15 – 30 years. Due to the way that banks amortize your mortgage payments, you’re paying mostly interest and only a small bit of principal during the first half of your home loan term. Here’s more info about how your credit score affects your interest rates.

Credit Score

Your credit score is only of the factors that goes into determining your mortgage rate but it’s one that pretty universal for borrowers so it makes sense to work on it. Improving your credit is a great way to reduce what you pay in interest.

Work to boost your credit score by making on time payments, reducing your debt, and being choosy about the new debt that you apply for. Remember, when you apply for a home loan it shows up on your credit report, so it’s best to check your credit first before just applying for a loan and seeing what rate you’re quoted. If it’s lower than you’d like, you can work to raise your score before filling out any loan applications.

When you have a good score, you should be able to qualify for a lower interest rate. So this should help you buy more house with less – since less of your payment will be going to interest. Saving up for a sizable down payment can also help, since you will be financing less of the home’s purchase price, and you will pay less in interest over time.

Credit score & Mortgage Rate Resources:

- How to Find the Best Mortgage Rates

- 12 Steps to Improve Your Credit Score

2) Home Bargain Hunting

All you have to do is drive around a few subdivisions and you’ll see the toll the housing market crash took on people who borrowed more than they could afford or who lost their job in the bad economy.

This has led to many foreclosures and short sales, which sometimes give you a chance to buy more house for less. Obviously this is bad news for existing home owners but can be an opportunity if you’re looking to buy a house for a bargain. According to CNN Money, foreclosures and short sales accounted for 26% of the total homes sold last year. Based on a recent RealtyTrac report, their statistics show that foreclosures save you an average of 36% off regular home prices – and short sales typically get you a discount of 15%.

How to Use Home Savings

A 15–36% discount on a $100K-$200K house can certainly save you a lot of money. The question is do you use that discount to spend your existing budget on a bigger home, or get a smaller house and pocket the savings? One thing to keep in mind is that if you’re buying a home that’s bank owned or in the process of foreclosure you’ll likely have to invest some money into it on top of the sales price.

Often home like these have been sitting empty for a while, which can cause problems for you as a new owner. For example, if the utilities have been turned off then there’s nothing to power a sump pump and spring rains can mean wet and moldy basements. Unfortunately, lack of care and maintenance isn’t the only concern. Sometimes previous homeowners that are being kicked out by the bank will take their anger out on the house and intentionally damage the property before leaving.

How Much Will a Bargain Cost You?

There can be some unexpected costs when buying a foreclosed home, however, there are ways to anticipate some of them. If you’re buying a house on the courthouse steps, which is an option right after a home has been foreclosed on, then it’s often sight unseen. You have to bring cash to the auction and when you buy the house you may not know all it’s potential issues.

However, if you buy a home from the bank that foreclosed on the property then you have more time to do some research and anticipate your costs. You can setup a time with the seller’s agent to bring in contractors to assess the damage and give you bids on what it would cost to get the house back into shape. Not only does this information help you figure out how much you can afford to pay for the home and still do repairs, you can also include the estimates in your offer to the bank to justify the price that you offer.

Non-Foreclosure Bargains

If you don’t want to deal with a foreclosed home, there are still ways to save money on a house. Start off by searching for homes that have been on the market for a while. What you’re looking for are listings that indicate that the seller is motivated to sell since that gives you room to negotiate.

One frequent cause of this are home owners who are moving to a new home and don’t want to be stuck with two mortgage payments. They may be more likely to give you a discount on price and get it sold than risk owning two houses for an extended period of time.

Some companies that relocate their employees will actually guarantee them a sales price for their home if they’re willing to move. Many of these companies work with re-location services to help sell homes and these can be a source of good deals for you. The company isn’t in the real-estate business and doesn’t want to hang on to mortgage debt, they’re motivated to sell the house quickly, which gives you an opportunity to negotiate the price.

Short Sales

As I mentioned earlier, short sales are another alternative to foreclosures. In these cases the bank hasn’t repossessed the property but the homeowner has asked the bank to let them sell the house for less than the amount owned on their loan.

The downside to short sales is that any offer you make has to be approved by both the home owner and the bank. Banks are so swamped with short sales that it can take forever for you to get a response on an offer. However, you can check the public records on a home and if you can find date it’s scheduled to go into foreclosure, this can give you leverage.

It’s often in the best interest of the property owner and the bank to get the home sold before going through foreclosure. So if the home owner is coming up against a foreclosure deadline they may be willing to approve a pretty low offer, simply to avoid foreclosure. Of course the trick is the bank also has to approve your offer so don’t make it so low that they simply dismiss it.

3) Know the Market

Understanding the local real estate market is a huge advantage when you’re trying to buy a house at a bargain. For example, anyone who comes to buy in my neighborhood is likely to pay $20,000 less than what the owner originally paid because there are so many homes for sale — and those that have sold have done so at a discount.

Real Estate Agents

One way to tap into market knowledge is to work with a buyer’s agent. It’s best if you can work with someone who specializes in a certain area. For example, if you really like a specific neighborhood and can find a buyer’s agent who actually lives in the neighborhood then you’re more likely to have access to property insights that you wouldn’t find with a random real estate agent you found in the phone book.

Technology

Whether you use an agent or not, you still want to do your own research. The Web makes it pretty easy to keep your eye on developments in areas that you’d like to buy. There are websites that allow you to save search critiera with your desired price range and house features. They’ll send you emails when new properties are listed or when prices change on existing homes. If you subscribe to a service like that for a few months you’ll have a decent feel for what’s available and what it will cost you.

Something else to consider is making use of a mobile device when you’re out “in the field” doing your research. A lot of information about real estate is now accessible via your smart phone so if you run across something new or unexpected while out looking at homes you may be able to do your research and get your question answered while you’re in a house or sitting out front in your car.

Buying More House For Less

If you can lower your borrowing costs and find real estate that’s “on sale”, it’s definitely possible to get more home for your money. Both of these require research, planning, and doing a fair amount of work before the actual purchase of a home. However, the money you’ll save will make your efforts well worth the time you invest.

What You Really Want

April 23, 2011

When was the last time someone sat you down and asked what it was you really wanted? I’ve done that with some of you over the last few months and I think it’s starting to pay off.

It all started when I was stuck in traffic one day, grumbling to myself about how I hate commuting downtown. Spending part of every day crawling along the highway wasn’t really how I wanted to spend my time – “but no one asked what I wanted”, I thought to myself.

Here are Your Options…

This started me thinking that in our daily lives no one asks us what it is we really want. Whether we’re at work, at the store, at the gym, or just out to have fun – we’re offered lots of options but no ever asks what things we want more than anything else.

We’re allowed to choose from what’s on the menu, the approved list, the available spots, the monthly specials, the rate plan, etc. But we don’t get to talk to someone and say, “all that other stuff is great – but this is what we really want”.

So I decided to ask some of you what purpose you wanted money to serve in your life. Your responses have been thorough and detailed and I really appreciate you taking the time to share. There are thousands of articles I could write about hundreds of personal finance topics but I want to be sure to include the ones that matter most to you.

What You Want

In a way, this is kind of a selfish request from me. If you’ve ever walked through the finance section in Barnes and Noble, you know from the rows of books that I could sit down in the morning and start writing about personal finance topics and write all day long every day and never cover everything.

Of course that would never happen because I have to go to work every day and our two little kids never let me sit very long when I’m home and they’re awake. However, even if I did have 24 hours a day to write I’d rather just talk about the things most important to you.

So what are these things? I’ve compiled all your feedback so far and the things you want to hear about most are:

- Investing

- Buying / Owning a home

- Saving for College

- Earning Extra Money

- Retirement Planning

You gave me a lot more detail on the specific types of issues you want to resolve but this these are the topics at a high level. If you haven’t had a chance to share but would like to have your topic considered you can still answer the 3 questions here. The answers are anonymous so you don’t have to feel self conscious sharing your story and issues. Most people have gone into detail and really opened up so don’t be shy : )

Coming Up

So in the coming weeks I’m going to run a series of posts around these topics. It was one year ago last week when we first met with our real estate agent and started the process of selling, then buying a house in one of the worst real estate markets in history. I’m glad weren’t not going through that again this summer but the experience is still fresh in my mind so we’ll start off by covering your real estate questions.

After that we’ll go through investing, paying for college, earning extra money, and retirement planning. Since summer is coming up, I’ll give you a little break from all the finance content and throw in a week about saving money on vacation.

Like I mentioned, if there’s something specific to those topics that you’d like covered, or something else I didn’t mention then answer these 3 questions and we’ll add it to the list. Now that you know what’s coming up on Money Smart Life, check out what went on with money this week on the web.

Frugality

- Find Your Treasure at a Freecycle Event @ Lazy Man & Money

- How To Keep Eating Well On a Budget @ Generation X Finance

- Saving Money with PaperBackSwap @ Beating Broke

- Balancing Frugality and Fun @ Rainy Day Saver

- How To Be Frugal And Not Lose Your Social Life @ Cool to be Frugal

Taxes

- How to File a Tax Extension 2011 @ Suns Financial Diary

- Last Minute Tax Tips @ My Dollar Plan

Personal Finance

- What To Do When You’ve Got Too Much Debt @ The Digerati Life

- chinese water torture @ Brip Blap

- The Dark Side of Gift Giving @ Frugal Dad

- 5 Online Career Resources for Moms @ Wisebread

- 72 Questions to Find the Perfect House @ Fiscal Fizzle

- Claiming a Canceled Debt as Income @ Little House in the Valley

- How to Spend Your Way to Happiness @ Get Rich Slowly

Insurance

- Eliminating Preexisting Conditions in Health Insurance @ My Dollar Plan

- All About a Health Savings Account (HSA) @ Budgeting in the Fun Stuff

Investing

- Types of Stock Charts @ Million Dollar Journey

- Dividend and Conquer @ The Wealth Artisan

- Being an Active Investor is a Lot of Work @ Free Money Finance

- What is the Stock Market? @ Moolanomy

- Working with Financial Advisors @ Consumerism Commentary

- Investing in the Face of High Inflation @ The Oblivious Investor

- The Three Legged Stool of Retirement Planning @ Saving Money Today

Also, thanks to the following sites for featuring our posts in the Carnival of Personal Finance:

- How to Improve Your Credit Score @ Money Management

- 12 Steps to Improve Your Credit Score @ Financially Digital

Wanting What You’ve Got

March 13, 2011

You know you’re getting older when you start listening to radio stations featuring music from 15 years ago. Last weekend, I really enjoyed an internet radio station that played only songs from the years I was in high school, brought back memories but also made me feel old.

After that ended the station started playing songs from early 2000 and one came on that I hadn’t heard for a while. The songs were mostly backround music but this one song, this one lyric caught my ear. When I heard it, I realized how true it was and how much of a difference it could make in someone’s life.

The song was “Soak Up the Sun” by Sheryl Crow and the lyric says:

“It’s not having what you want

It’s wanting what you’ve got”

Having What You Want

The pursuit of having what you want is one that can lead to eternal disappointment. For whatever reason, us humans seem to be wired to always want more than we have.

This isn’t necessarily a bad thing, this drive to achieve is what helps many of us excel in life. This internal force is the momentum behind countless acheivements where people accomplished things they were told couldn’t be done.

Pioneers in all areas of our society have had big dreams, have had enormous “wants” and pursued those relentlessly. Innovation and growth have helped to propel the “American Dream” for hundreds of years. That dream has changed from generation to generation but a common theme has been to make a better life for ourselves, our families, and our community.

There’s no doubt that the struggle to have what you want for you and your family can be exhausting. I think one of the reasons for this is that we keep resetting the standard that we strive to meet. We achieve our goals, then look ahead to the next milestone of our American dream.

One of the things that happened along the way is that people discovered they could get what they wanted sooner by borrowing money to pay for it. It became possible to spend money we don’t have and after a while we found ourselves working to pay the interest on the American dream that we had paid for pre-maturely – before we could actually afford it.

Wanting What You’ve Got

So back to the lyrics, “it’s not having what you want – It’s wanting what you’ve got”. There’s nothing wrong with ambition and the desire to grow and excel but if we can’t take time to appreciate where we’ve come from and what we’ve acheived – then we spend our whole life trying to get what we want.

This can be tough to do, I struggle with this myself. I have big dreams and big plans so sometimes I have to stop and remind myself of the blessings I have in life. I don’t think I’ll ever be able to squash the voice in my head that drives me to improve and create but I have to make sure that I take time to “want what I’ve got”. What do you think? Is it easier said than done, or are you pretty content with your spot in life?

Anyhow, not that I’m finished with my financial reflections, here are some articles from the week you might enjoy:

Personal Finance

- Lending Club Update @ Lazy Man & Money

- Financial Lessons From Charlie Sheen @ Suns Financial Diary

- Can You Afford It? @ My Dollar Plan

- Don’t be Milton @ Brip Blap

- Why We Crave More Stuff @ Frugal Dad

- What’s Your Financial IQ? @ Moolanomy

- Paying Off Debt With Pizza @ PT Money

Investing

- This is Why You Can’t Make Money in the Stock Market @ Generation X Finance

- Cheap Ways To Buy Dividend Stocks @ The Digerati Life

- A Primer on Mutual Fund Fees & Sales Load @ Million Dollar Journey

Also, thanks to Own the Dollar for recently including Money Smart Life in the carnival of Credit Score and Debt and to Kid Money for our inclusion in the Family Finances carnival.

Saving Money in Crazy Ways – Carnival of Personal Finance #297

February 21, 2011

Even though the recession is technically over, many of us are still looking for creative ways to save money. Or at least make more money. Or better our finances. This Carnival of Personal Finance highlights great ways to improve your personal economy — no matter what the national economy is doing. Most sections has a video of crazy things that people do to save money. Enjoy!

Editor’s Choice

Here are a few posts I found especially helpful this week.

- Who has your personal financial information? Prairie Eco Thrifter has 8 ideas for protecting yourself from ID theft.

- Squirrelers really puts things into perspective by helping you see how many hours you are working to buy your stuff. Eye-opening. And a little depressing.

- A Gai Shan Life presents an interesting look at the financial (and emotional) issues that can accompany having your parents move in with you.

- Dealerity is taking a challenge to live near the Federal poverty line for a month. It’s a fascinating challenge, and I also found his update for Day 15, focusing on accepting help from others, quite interesting.

- Moneyed Up offers some good advice on how you can be good at what you do — whatever that is.

Budgeting & Money Management

It’s important to consider your budget. This means planning your spending and doing your best to avoid buying things you can’t afford.

- If you are looking for help with your financial goals, You Have More Than You Think offers you an idea of what your #1 tool could be.

- As your net worth calculations become too complicated, Money Beagle asks if perhaps you should ditch the earmarks you have been using.

- First Generation White Collar shares some thoughts on why financial willpower is so difficult to come by — and what you can do to get beyond it.

- Let’s get real. Couponing may not always save your finances. Sometimes you have to sweat the big the stuff, insists Moolanomy.

- Net Worth Journey helps you understand how debit card transactions work.

- Set a good example and teach your children something worthwhile. Christian Personal Finance offers good ideas for helping your kid buy a car.

- Matt About Money takes principles from the business management classic Good to Great and applies them to personal finance.

- Len Penzo dot Com offers a look at the Personal Finance Anarchist Cookbook. Watch out for these dangerous money items.

- Money Walks presents some ideas for keeping your food budget under control.

- Activity isn’t always the same as achievement. This is true in money management, insists THE Canadian Finance Blog.

- Do you have a variable income? The Dough Roller provides insight on budgeting in such situations.

- Adjust your budget to cope with rising food prices with some help from Modern Gal.

- Review of best personal finance software. One Money Design helps you find a program to keep you on the right track.

Career

What sorts of decisions are you making with your career? Are you impressing others with your good ideas? Or have you neglected to think things through?

- Looking for a legitimate work from home job? Living Richly on a Budget looks at the site FlexJobs.com as a source for telecommuting jobs.

- If you want to start your own business, this post on using your IRA for that purpose is a helpful resource from Good Financial Cents.

- Personal Cents provides practical insights on being self-employed.

- What if becoming a stay at home parent is the next step in your career? Well Heeled Blog takes a look at what you need to know.

- Dividend Stocks Online helps you figure out when you can retire. The ultimate in career goals.

Credit & Debt

Running up debt? Spending on credit instead of saving? Here are some things to think about.

- You never can be too careful. You want to save money on credit card interest, but Credit Card Assist Blog points out that you might be heading into a rate reduction scam.

- Someone is always trying to part you from your money. Consumer Boomer offers you a look at these debt relief scams to be wary of.

- Know your rights. The Credit Card Forum Blog shares some of the legalities behind whether or not credit cards companies can sue you.

- Even good debt can go bad, points out Money Help for Christians.

- Learn how to pay off debt quickly with some tips from Accumulating Money.

- Find out how you can get a free credit score when you read The Sun’s Financial Diary and a take on Credit Sesame.

- Free From Broke reviews the Platinum Card from AmEx.

- It’s hard to stay motivated when trying to pay off debt. PT Money offers some encouragement.

- It would be great if debt free living was good for your credit score. Unfortunately, points out Canadian Finance Blog, it’s not.

- Learn how you don’t need a personal guarantee for a business credit card at CardHub.com.

- Gen X Finance talks about how to

- NerdWallet Credit Card Blog cautions readers against buying extra AAdvantage Miles.

- Is Yes I Am Cheap crazy for purposely adding $20,000 to credit cards?

- Lazy Man looks at how to get a free credit score.

Economy & Finance

In this tough economy, it’s important to find ways to save money, from saving energy in the home to saving money on transportation. How are you dealing with the economy?

- Did you inherit an IRA? New IRA Rules offers a helpful look at what you need to know about an inherited IRA.

- Why is wage inequality on the rise? Don’t Quit Your Day Job offers an explanation of the economics behind wage differences.

- Can you really trust financial simulations? The Oblivious Investor takes a look at the situation.

- The children are our future. Barbara Friedberg looks at the importance of teaching financial lessons to your kids.

- There are special financial challenges when you are in the military. Compounding Interest takes a look at finances and military members.

- Darwin’s Money provides you with a look at the difference between financial accounting and managerial accounting.

- Food inflation is coming. Financial Uproar wonders if you’ll even notice.

- If you are a common consumer, Money Thinking offers a helpful look at deal-making and the price mechanism.

- Are you ready to recognize the truth about your financial situation? Until you do, points out Hope to Prosper, you won’t be able to make solid progress.

- The Military Wallet warns that military personnel had better get used to fee increases to TRICARE Prime.

Frugality

There’s nothing more frugal than free. But, free isn’t always an option. Here are some articles that will help you live a little more more frugally.

- A new addition to the family on the way? Fiscal Fizzle offers a look at 10 things you can do to save money on a new baby.

- Protect your home, fortifying it against would-be intruders. Live Real, Now tells you how to do it frugally.

- Is it such a good thing that everyone is talking about “frugal fatigue?” Surviving and Thriving is a little worried about what it could mean to trivialize the idea of frugality.

- The Red Stapler Chronicles shares the personal finance hall of shame.

- Want to save money? Grumpy Rumblings of the Untenured says that sometimes it’s as easy as asking.

Investing & Real Estate

What sort of investments are you making? How do you scrape together the money to invest more, anyway?

- With a good brokerage firm, points out Qwoter, you can get better returns..

- Green Panda Treehouse can help you learn a little bit more about exchange-traded funds.

- Once you have learned the basics of ETF investing, Experiglot can help you figure out ETF allocation.

- Shareholders of Google might be interested to know about the new CEO, Larry Page. Intelligent Speculator is ready to provide a little background.

- For most ordinary investors, marketing timing is probably not the best investment strategy. The Dividend Guy Blog tells you why marketing timing might be a bad idea.

- Young? Interested in investing? Do Not Wait offers tactics that can help you find investing success.

- If you pick right, according to Compounding Returns, your long term stock investing strategy can pay off big.

- Interested in a solid retirement vehicle? Smart On Money explains why the Roth IRA is a popular choice.

- Investor Junkie offers a review of the online broker TradeKing.

- Back Nine Finances shares the process of looking for an income property.

- A great interview with an energy fund manager from Investing Thesis.

- An overview of different types of mutual funds from Buy Like Buffett.

- Learn more about timing your stock trades with help from The Digerati Life.

- The Smarter Wallet encourages you to own stocks for long enough to make a profit on them.

- Emerging markets are enjoying a boom. Retire Happy looks at emerging market investing.

- Learn how to maintain your asset allocation as new funds come in from Dividend Growth Instructor.

Taxes

You want to save all the money you can when it comes to what you owe the government. After all, it’s about keeping what’s yours anyway.

- Want to know the difference between married filing jointly and married filing separately? Bargaineering gives you a crash course in filing status.

- If you adopted in 2010, Spruce Up Your Finances can help you navigate the adoption credit on your tax return.

- Want another chance at a tax deduction? Bible Money Matters points out that you can still open an IRA for 2010.

- Curious about whether or not credit card rewards are tax deductible? My Dollar Plan has an answer.

- Wallet Blog points out that even if you are unemployed, you still have to pay taxes — and on your unemployment income.

Other

In the end, how you save money says a lot about you. How do you keep from spending too much?

- Free Money Finance continues to struggle with Sears. The latest in the epic battle between company and customer.

- Learn how to follow worthwhile wealth creators on Twitter with these tips from Money Cactus.

- Find out the basics of if you need travel insurance from Help Me Travel Cheap.

- Saving to Invest offers a primer on the importance of life insurance, and how to choose the right option for you.

- Want to know more about the costs and benefits of the Samsung Epic? Budgeting in the Fun Stuff offers a review.

- You can your cash out your prepaid debit card. Growing Money shows you how.

- Consumerism Commentary asks readers the question: Are you better off than your parents?

- Is there a link between money problems and domestic violence? Cash Money Life explores the possibility.

Next Carnival will by hosted by Saving to Invest. Be sure to get your submissions in using the form.

Free Financial Advice 2011

January 24, 2011

One of the best things my wife and I did for our money after we were married was sit down with a certified financial planner and hash out our finances. I remember we weren’t crazy about spending the money but after we worked with our finanial advisor to come up with our financial plan we knew that it was money well spent.

If you’ve been thinking about working with a financial planner but don’t want to spend the money you have a chance tomorrow to get a free consultation with a fee only financial planner. It’s not a full blown financial planning session, you just get one question, but it can give you a feel taste of what a financial planner can help you with.

Here’s a blurb from the Kiplinger website:

“Kiplinger.com is hosting a live discussion with members of the National Association of Personal Financial Advisors (NAPFA) for Kiplinger’s Jump-Start Your Retirement Plan Days. From 9 a.m. to 6 p.m. eastern time, these fee-only planners, who are well versed in investments, taxes, insurance, estate planning, and saving for college and retirement, will take questions. The NAPFA planners will answer as many questions as time permits.”

Sounds like it’s first come, first serve so call in early and check it out.

Here are some personal finance articles from around the web this week

Personal Finance

- From homelessness to success @ Brip Blap

- What Determines Value? @ Couple Money

- Average American Family’s Finances: In Shambles? @ The Digerati Life

- Financial Goals for 2011 : What are Yours? @ Million Dollar Journey

- Series: Life After Salary @ Consumerism Commentary

- 11 Lesser Known Finance Blogs to Read in 2011 @ Moolanomy

- 4 Money Mistakes to Fight in 2011 @ Bible Money Matters

- How to Make Your Financial Goals a Reality @ Free From Broke

- Isn’t It Easier to Read About a Success Story Than Do It? @ Eventual Millionaire

Frugality

- Thred Up Because Kids Outgrow Clothing Fast @ Generation X Finance

- How to Do Tactical Budgeting @ Good Financial Cents

- 9 Ways to Prepare for Food Inflation @ Frugal Dad

- Eating Healthy Is No Cheap Task @ Dough Roller

Deals

- Living Social Buying a Million Customers? @ Lazy Man & Money

- $20 Amazon.com Gift Card for $10 at Living Social @ Suns Financial Diary

Investing

- Investment Returns Vary Over The Long Run @ My Money Blog

- How Much Income Will You Need in Retirement? @ The Oblivious Investor

- How Warren Buffett Invests @ Investor Junkie

Thanks to Living Richly on a Budget for hosting my post, Free Credit Scores – Coming Soon in the latest carnival of personal finance.

Vacation Without Kids

January 16, 2011

With all the talk of rental car insurance and rental car rewards you might have been able to tell we’re going on vaction. This is a monumental one, it’s the first time we’ll have been away from our daughter for more than a night since she’s been born.

Our son is excited to visit his grandparents and be spoiled so he didn’t shed a tear when we told him we were leaving. Although we’ll really miss our kids it will be nice to get away. We’ll actually be able to have a conversation without being interrupted by a barrage of questions or a crying kid.

As usual when leaving for vacation, I’m running behind so I’ll just leave you with a few articles to check out this weekend.

Investing

- Avoid Stock Market Losses! Beware Of These 5 Investment Mistakes @ The Digerati Life

- Five Ways to Maximize Your Retirement Accounts @ Five Cent Nickel

- Stocks or Mutual Funds: Which Should I Buy? @ The Oblivious Investor

Taxes

- Why Your Tax Withholding Went Up @ Bargaineering

- Will You Be Subject to the IRS Tax Filing Delay? @ My Dollar Plan

Personal Finance

- tips for staying financially fit in 2011 @ Brip Blap

- 2010 Financial Goals Evaluation @ Million Dollar Journey

- How to Overcome a Financial Loss @ Cash Money Life

- Credit Sesame: Free Credit Scores & Debt Management @ Lazy Man & Money

Frugality

- 5 Lessons Dave Ramsey Taught Me About Healthy Living @ Frugal Dad

- 3 Ways to Save Money On Sleepwear Like Pajamas @ Money Ning

- Revamping Your Budget for the New Year @ Being Frugal

Insurance

- Why You Need an Umbrella Insurance Policy @ Free Money Finance

- Putting Your Teenage Son or Daughter on Your Auto Insurance Policy @ Generation X Finance

Thanks to the following sites for including mentions to my articles:

myFICO Review

January 11, 2011

myFICO is the consumer credit score site of the creator of the FICO credit score system, Fair Isaacs. You have several options on the myFICO site for finding your FICO score online and monitoring your FICO score. myFICO does charge for access to your score but offers a free credit score trial to let you check out their ScoreWatch service. You can also find occasional discounts via their myFICO promotions.

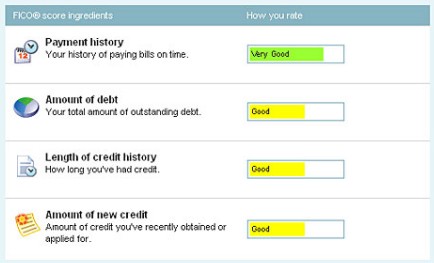

myFICO & Your Score

You probably already know that your FICO score is the credit score that many lenders — and even some insurance agents and employers — use to determine what sort of financial risk you represent. Variations of the FICO score are used in a number of ways to determine approval and rates for your mortgage, car loans, and credit cards. However, the FICO score is used by 90% of the largest banks and 100 of the top 100 U.S. credit card issuers so it’s the heavy hitter when it comes to credit scores.

myFICO Standard

At the most basic level you get your FICO score, plus receive an explanation about what it means and an idea of how lenders view you.

You can choose to see your FICO score from either TransUnion or Equifax, Experian no longer participates. FICO standard also includes a credit report from TransUnion or Equifax, whichever FICO score you choose – your score will likely vary somewhat across credit bureaus.

The FICO Standard score and report is $19.95, but as mentioned earlier you can see your credit score and credit report at no charge if you sign up for a free trial of ScoreWatch.

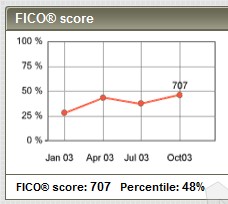

myFICO ScoreWatch

ScoreWatch allows you to get two FICO scores and two credit reports from Equifax each year, and it keeps tabs on changes to your credit score.

If you’re looking for the trending of your FICO score rather than just a snapshot then Scorewatch can be useful. For example, if you’re trying to improve your credit score and want to see progress, ScoreWatch gives you a graph of your score over time as well as regular updates:

- Monitors Equifax credit report daily & FICO score weekly

- Target credit score notifications

- Notifications when you qualify for a better interest rate

- FICO score drop alerts due to changes in your credit report

FICO Quarterly Monitoring

If you’re not actively tracking your credit score but want to check in on it a few times a year, FICO Quarterly monitoring can help you keep tabs on your score.

As you may know you’re able to get a free credit report every year from each credit bureau from annualcreditreport.com. This service uses TransUnion and makes your credit report and credit score available every quarter. The one extra credit report you get from the myFICO service is nice but you might not really feel like you need it. The main benefit of this service is that you get your credit score in addition to your credit report.

So every three months you receive a score and report, and an explanation of the positive and negative items affecting your score. You can identify problem accounts, as well as look for ways to improve your credit situation. The Quarterly Monitoring service will also alert you to changes in your credit score.

In the event that the change was due to identity theft, myFICO’s Quarterly Monitoring also provides identity theft insurance for up to $25,000 and a hotline to help you file id theft reports and complaints.

Suze Orman’s FICO Kit

While ScoreWatch and Quarterly Monitoring are setup to keep track of your credit score over time, the Suze Orman FICO kit is designed to walk you through the steps to help improve your credit. Created along with personal finance author Suze Orman, there’s more coaching and what-if analysis in the FICO kit.

Suze Orman’s FICO Kit gives you three credit reports and scores a year. The kit also includes the FICO Kit Action Planner that helps you take the information in your credit report and plan out steps to improve your score.

You can tailor the tool to your personal situation with their tools like the debt eliminator, bill pay reminders, and online coaching to help you get a car loan or home loan are included. You can also use the FICO Simulator, which allows you to estimate the effect certain changes would have your score.

You can use this myFICO promo code to get a discount on the FICO kit – SUZEFKP

Just for Kids Weekend

October 10, 2010

Our kids had an awesome weekend! The weather was perfect here in the Midwest and we knew before long our little ones would be cooped up by the winter weather so we let them enjoy the outdoors. I think a local festival and neighborhood carnival were the highlights of our son’s weekend. Although they had a blast we didn’t really didn’t get anything done since we spent the whole time chasing them from one fun event to the next. It could be a late one, playing catch-up on work tonight but they had fun so it was worth it.

Here are some articles you should check out, seems like the Frugality section is always one my biggest. I guess it’s just because I love saving money!

Investing

- Correlation: The Reason For Asset Allocation @ Investor Junkie

- Asset Allocation for People in their 20s @ Sweating The Big Stuff

- Best Books on Investing: My Favorite Investing Authors @ Get Rich Slowly

- Asset Allocation Strategies: Rebalance Your Portfolio @ The Digerati Life

Credit

- Five Tips To Establish Credit! @ Millionaire Nurse

- Don’t Forget to Opt-In for Your 5% Cash Back Rewards @ Nerd Wallet

- Guaranteed Ways To Lower Your Credit Score @ Free From Broke

- How to Freeze Your Credit Report at All Three Credit Bureaus @ Generation X Finance

Frugality

- Layering Your Deals @ Frugal Confessions

- Spend Less on Baby Formula @ Money Ning

- Save Money on Dining Out Expenses @ PT Money

- 20 Ways to Save Some Cash @ Budgeting in the Fun Stuff

- Doing the Math on Refilling Ink Cartridges @ The Simple Dollar

- Mastering Negotiation to Save Money @ Suns Financial Diary

- 6 Ways to Change the Impact of Food on your Budget @ My Dollar Plan

- Frugal Entertaining Without Breaking Your Budget @ Eventual Millionaire

- How to Avoid Christmas Debt Without Becoming a Grinch @ Personal Finance By The Book

Personal Finance

- The Financial Toll of Special Diets @ Beating Broke

- Financial Lesson For My Son: Savings @ Money Reasons

- Ways to Track your Spending @ Million Dollar Journey

- Five Daily Activities to Improve Your Finances @ Frugal Dad

- Paperless Office: The Secret Savings @ Lazy Man & Money

- Is the Troubled Asset Relief Program (TARP) Working? @ Dough Roller

- 3 Reasons Why Spreadsheets Make Effective Tools @ Fiscal Fizzle

- Saving Money on Your Phone Bills with Microsoft Excel @ Couple Money

- Decision-Making Difficult for Ambivalent People @ Consumerism Commentary

Retirement

- Planning Your Retirement Spending @ The Oblivious Investor

- The Perils of Pursuing Financial Freedom @ My Money Blog

- An Example of Early Semi-Retirement @ Free Money Finance

Career

- Should I take a Pay Cut? @ Brip Blap

- 14 Resume, Cover Letter, and Application Mistakes to Avoid @ The Money Crashers

Announcements

Baker from Man vs Debt offers a few great guides to selling your stuff on eBay and Craigslist in his recently released course – Sell Your Crap.

Matt Jabs at Debt Free Adventure has launched a cool initiative aimed at helping yourself and others. You can hear more about it in his DFA Missionaries video.

Jeff Rose at Good Financial Cents announced the title of his upcoming book, Soldier of Finance.

Congrats to those guys for making things happen. Also, thanks to the following carnivals for including our post.