Free Financial Advice 2011

One of the best things my wife and I did for our money after we were married was sit down with a certified financial planner and hash out our finances. I remember we weren’t crazy about spending the money but after we worked with our finanial advisor to come up with our financial plan we knew that it was money well spent.

If you’ve been thinking about working with a financial planner but don’t want to spend the money you have a chance tomorrow to get a free consultation with a fee only financial planner. It’s not a full blown financial planning session, you just get one question, but it can give you a feel taste of what a financial planner can help you with.

Here’s a blurb from the Kiplinger website:

“Kiplinger.com is hosting a live discussion with members of the National Association of Personal Financial Advisors (NAPFA) for Kiplinger’s Jump-Start Your Retirement Plan Days. From 9 a.m. to 6 p.m. eastern time, these fee-only planners, who are well versed in investments, taxes, insurance, estate planning, and saving for college and retirement, will take questions. The NAPFA planners will answer as many questions as time permits.”

Sounds like it’s first come, first serve so call in early and check it out.

Here are some personal finance articles from around the web this week

Personal Finance

- From homelessness to success @ Brip Blap

- What Determines Value? @ Couple Money

- Average American Family’s Finances: In Shambles? @ The Digerati Life

- Financial Goals for 2011 : What are Yours? @ Million Dollar Journey

- Series: Life After Salary @ Consumerism Commentary

- 11 Lesser Known Finance Blogs to Read in 2011 @ Moolanomy

- 4 Money Mistakes to Fight in 2011 @ Bible Money Matters

- How to Make Your Financial Goals a Reality @ Free From Broke

- Isn’t It Easier to Read About a Success Story Than Do It? @ Eventual Millionaire

Frugality

- Thred Up Because Kids Outgrow Clothing Fast @ Generation X Finance

- How to Do Tactical Budgeting @ Good Financial Cents

- 9 Ways to Prepare for Food Inflation @ Frugal Dad

- Eating Healthy Is No Cheap Task @ Dough Roller

Deals

- Living Social Buying a Million Customers? @ Lazy Man & Money

- $20 Amazon.com Gift Card for $10 at Living Social @ Suns Financial Diary

Investing

- Investment Returns Vary Over The Long Run @ My Money Blog

- How Much Income Will You Need in Retirement? @ The Oblivious Investor

- How Warren Buffett Invests @ Investor Junkie

Thanks to Living Richly on a Budget for hosting my post, Free Credit Scores – Coming Soon in the latest carnival of personal finance.

Angies List Discounts

Angies List discounts are available periodically via coupon codes or promo codes – I just ran across a new Angies List promo this week. This one is actually through a partner, the Angies List deal is available if you’re a member of the site BULX.

It only runs for a few days but you can get an Angies List membership discount of 40% through their promotion. BULX is kind of like Groupon for furniture, I haven’t really seen many partner deals from Angies List but this one is a cool idea. I got the email announcing it since I’m a member, here’s what the page had to say about the service:

- Reviews are submitted by verified members, not anonymous visitors.

- Companies don’t pay to be on Angie’s List.

- The only review site certified annually by BPA Worldwide, a respected auditing firm.

- Find and submit reviews in more than 500 service and health care categories including plumbers, roofers, dentists, and medical specialists.

- See both sides of the story: Companies and providers can respond to their reports.

We’re members and I gave away some free Angies List memberships a while back to let some of you try it out. I’ve written before about some of the ways we use the service to find local contractors but another benefit I’ve never really mentioned is that they give you a heads up on scams to watch out for in your area.

Since they get so much good and bad feedback on local companies they keep track of common problems and send out summaries via the Angies List magazine. For example, last year they highlighted air duct cleaners who lured customers with too-good-to-be-true coupons, false advertising locksmiths, real estate short sales scammers, aggressive door-to-door alarm salesmen, and Internet car sales scammers.

Anyhow, if you’ve read about the service here before and ever thought of trying it out, you can get a pretty big discount.

Southwest Rapid Rewards Plus Card – 2 Free Flights

The Southwest airlines credit card is one of the highlights of the new Rapid Rewards program from Southwest. I flew Southwest this week and learned that the new Rapid Rewards program will be based on points instead of miles and the Southwest rewards card offers ways, other than flying, to earn those points.

Southwest Rapid Rewards Points

Apparently one of the benefits of Southwest using a rewards points system is that it’ll be easier for the rewards program to add more partners into its network. The points make it simpler than the system of credits to work with partners to offer travel rewards.

While there’s been a mixed reaction to the new rewards program, the ability to earn more points with the Southwest card has been one of the areas that Southwest customers are most pleased with. You earn two points for every dollar spent on Southwest tickets or with Southwest Rapid Rewards partners.

Southwest Rapid Rewards Partners

The primary Rapid Rewards partners right now are the hotel chains and car rental companies below:

- Rental Cars (Alamo, Avis, Budget, Dollar, Hertz, Thrifty)

- Hotels – Best Western, Hilton Honors, Hyatt, La Quinta, Marriott, Starwood Preferred Guest, Wyndham, Choice Hotels International

These partners all earn double points and you’ll also earn an additional 600 points per stay at Rapid Rewards hotel partners. Some of these hotels, like Marriott and Starwood, have their own rewards cards but people that fly Southwest frequently will likely prefer the Southwest rewards.

One of the changes in the new Southwest rewards program is that points don’t expire like they used to. As long as you fly every 2 years or use one of these partners every 2 years your rewards points don’t expire.

Southwest Rapid Rewards Dining

You can also earn rewards in the rapid rewards dining program. To participate in dining rewards program you register your card on the Rapid Rewards Dining site and earn points when you eat out at restaurants or bars in the dining rewards network. You can search for local restaurants by zip or address on their site.

The card you register doesn’t actually have to be the Southwest credit card; it can be any American Express, Discover, MasterCard, VISA credit card or even a debit card. Once you’ve accumulated enough points in your rewards dining account they transfer it over to your rapid rewards account.

If you do use the Southwest credit card from Chase then you’ll get an additional point per dollar spent. Earning one point for each dollar you spend is the standard rewards rate for purchases not made from Southwest partners.

Southwest Rapid Rewards Bonus

The Southwest Rapid Rewards card does have an annual fee ($69 Signature/ $99 Premier ) but you get 2 free flights when you sign up for the card and use it the first time.

I stopped by the signup booth to check out the card features on our return flight. I was able to ask a bunch of questions about the card and Rapid Rewards program but then our flight started to board so then all I had time for was this picture of the Southwest counter.

It’s probably easier to just check it out on the web anyhow. To read more about the details of the rewards and the card – check it out here.

Don’t Get Bamboozled Like These Professional Athletes

This is a guest post by Jeff Rose. Jeff Rose is an Illinois Certified Financial Planner and co-founder of Alliance Investment Planning Group. He is also the author of Good Financial Cents, a financial planning and investment blog and he is currently working on his first book entitled Soldier of Finance. You can see more about his mission at the same titled blog Soldier of Finance.com.

Let’s face it – most of us (especially if we’re men) have wanted to be professional athletes at some point in our lives. What a life! You make barrels of money to travel around the country, play a game you love, and talk to reporters about it. If you’re really good (or just really famous), you get all kinds of untold millions from TV appearances, speaking engagements, and product sponsorships. What life could be better than that?

It Doesn’t Make You Invincible

What we forget so easily is that professional athletes are not superhuman. They’re people like us. And no matter what the announcers say, no matter how unbelievably amazing the local papers make them out to be, they’re still just people like you and me. And they still have to be careful with their money.

John Elway Scammed

John Elway is a prime example. He invested $15 million with a hedge fund manager. Turns out, that hedge fund manager was actually running a ponzi scheme (like the famous Bernie Madoff scheme from earlier in 2009. A ponzi scheme is run by using invested monies to pay out to previous investors, but the money isn’t actually invested). Elway is a rare case though – he actually got back most of his money. But not before $3 million of it went missing down the tubes of a big lie.

Elway was one of about 65 people who had invested money with Sean Mueller, which totaled around 71 Million dollars. Near the time of his arrest, he only had about 9.5 million dollars left. Whoops.

Michael Vick Scammed

A similar thing happened to Michael Vick. Having invested with an advisor who worked with a number of other NFL players, Vick was part of an investment pool of $3 million dollars that was never invested in the high end luxury investments his advisor purported to sell. Instead of investing the money, Vick’s investor used it to support her other business ventures. Turns out, she was barred from trading securities in September 2007. Double whoops.

One of the many caught up in the Bernie Madoff ponzi scheme was baseball great Sandy Koufax. He and his high school buddy New York Mets owner Fred Wilpon, along with other people associated with the New York Mets all took a hit from Madoff. People like former mets infielder Tim Teufel, former owner of the Philadelphia Eagles Norman Braman, and former New York Islander Bob Nystrom. Also affected were Mets associates like Sterling Mets, The New York Mets Foundation, and the Mets Limited Partnership.

Should I keep going, or do you see my point?

Want me to tell you about how former New York Jets quarterback Mark Brunell went bankrupt through a series of bad real estate deals that ultimately landed him with $5.5 million in assets to pay of $25 Million in liabilities? What about NBA players like Antoine Walker? Or Derrick Coleman. Both bankrupt.

Being a professional athlete does not guard you against financial mistakes. Nothing does. But being a Soldier of Finance certainly helps.

Jeff Rose is an independent financial advisor who loves Crossfit workouts, writing about Roth IRA Rules and craves In-N-Out burger. You can follow his updates on Twitter: @jjeffrose.

Vacation Without Kids

With all the talk of rental car insurance and rental car rewards you might have been able to tell we’re going on vaction. This is a monumental one, it’s the first time we’ll have been away from our daughter for more than a night since she’s been born.

Our son is excited to visit his grandparents and be spoiled so he didn’t shed a tear when we told him we were leaving. Although we’ll really miss our kids it will be nice to get away. We’ll actually be able to have a conversation without being interrupted by a barrage of questions or a crying kid.

As usual when leaving for vacation, I’m running behind so I’ll just leave you with a few articles to check out this weekend.

Investing

- Avoid Stock Market Losses! Beware Of These 5 Investment Mistakes @ The Digerati Life

- Five Ways to Maximize Your Retirement Accounts @ Five Cent Nickel

- Stocks or Mutual Funds: Which Should I Buy? @ The Oblivious Investor

Taxes

- Why Your Tax Withholding Went Up @ Bargaineering

- Will You Be Subject to the IRS Tax Filing Delay? @ My Dollar Plan

Personal Finance

- tips for staying financially fit in 2011 @ Brip Blap

- 2010 Financial Goals Evaluation @ Million Dollar Journey

- How to Overcome a Financial Loss @ Cash Money Life

- Credit Sesame: Free Credit Scores & Debt Management @ Lazy Man & Money

Frugality

- 5 Lessons Dave Ramsey Taught Me About Healthy Living @ Frugal Dad

- 3 Ways to Save Money On Sleepwear Like Pajamas @ Money Ning

- Revamping Your Budget for the New Year @ Being Frugal

Insurance

- Why You Need an Umbrella Insurance Policy @ Free Money Finance

- Putting Your Teenage Son or Daughter on Your Auto Insurance Policy @ Generation X Finance

Thanks to the following sites for including mentions to my articles:

Best Credit Cards for Rental Car Rewards

The best credit cards for car rentals combine some or all the travel perks of car rental deals, rental rewards, and rental car coverage. The infamous rental car insurance episode on Seinfeld wouldn’t be so funny in real life – so here are some things to consider when searching for the best rental car credit card for your trip.

Car Rental Deals

Saving money is always important when you’re traveling so one thing to look for in a credit card is whether it can score you any car rental discounts. For example, the Blue Savings Program from American Express offers deals when you use your Blue Cash, Blue Sky, or AmEx Blue card to rent a car:

- 5% off on an Enterprise rental

- $20 credit after $200 in Enterprise rentals

- Up to 25% off Alamo rental

Other credit cards may send you periodic car rental coupons for certain companies like Alamo and Avis – my Bank of America Visa offers a regular discount at Hertz.

If you’ll be hauling around a bunch of people or stuff and need a bigger car you can also save money on upgrades. Another example in the Blue Savings program, you get a rental car coupon code for a free upgrade at Hertz or with Alamo.

Car Rental Rewards

In addition to discounts, you might also be able to earn rewards points or use them to help pay for your rental car.

Earning Points

The Marriott Rewards card gives you 2 points for each dollar you spend on rental car purchases – and with Hilton HHonors cards you earn 250 Hilton Honors points with each car rental at one of their partners (Alamo, Avis, Budget, National, Sixt, & Thrifty).

If you use an American Express card that participates in the Membership Rewards program, such as the American Express Gold Card or ZYNC from American Express you can earn double Membership Rewards Points when you book through the AmEx travel site.

You can also earn rewards points (or Starpoints) on the Starwood Preferred Guest card when you get your rental car from Avis. If you’re a preferred guest member and you use the Avis Worldwide Discount (AWD) code of K817200, you’ll also get a $50 discount on the car rental.

Redeeming Points

Some rewards credit cards let you use your points when you’re renting a car to help you get a discounted or free car rental. If you don’t want to go through your credit card company to book your travel, another alternative is to turn in your rewards for gift cards.

If you use any of the Citibank cards in the ThankYou Rewards program, like Citi ThankYou Premier or Citi Forward, you can redeem ThankYou points for gift cards at car rental companies.

Discover also lets you turn in your rewards for gift cards at Alamo, Enterprise, and National. If you use the Discover card and redeem your cashback earnings for a gift card, Discover will give you double the value of your rewards on the gift card.

Rental Car Insurance

The terms and conditions of credit card rental insurance vary based on the card you use so make sure you understand exactly what’s covered.

The Collision Damage Waiver offered by rental car companies can be pretty pricey – if you have primary coverage through your auto insurance company and secondary coverage through your credit card then you can probably avoid that charge.

When you’re renting a car, make sure you ask about any “loss-of-use” fees or “administrative processing” fees the rental company might charge if you have an accident. Be clear on what is covered by your credit card plan and your primary insurance before declining rental car insurance from the company.

Cash Back Rewards

We’ve looked so far at how you can save with car rental deals and earn/redeem rewards points. Another possibility is to take advantage of cash back rewards when you make certain purchases at rental car companies.

There are some cards that feature rotating cash back categories where you can earn 5% on those categories of purchases. If you can earn 5% cashback on car rentals when you’re traveling then it would be a good time to use a card with that feature.

Of course, if you’re not traveling during those months then the 5% cash back won’t do you much good. If that’s the case then you might want to look at cards like TrueEarnings from American Express, where you always earn a fixed cash back amount on travel expenses.

As I said at the start, choosing the best car rental credit card means looking at a combination of the deals you can get, rewards you can earn, and coverage you’ll have on your rental car. Hopefully this review of different credit card options will help you choose the best one for you.

10 Credit Card Rental Car Insurance Surprises

Does your credit card offer rental car insurance? In honor of Jerry Seinfeld using his only credit card that didn’t have rental car coverage, these are ten things you might not know about insurance when renting a car.

It all started when I rented a car recently with my Blue Cash card and I called in to see how the Car Rental Loss & Damage Insurance Plan worked for American Express.

If you’re renting a car with a travel rewards card from Visa or Mastercard you’ll need to check out the policy of your card but these should at least give you a few things to investigate and questions to ask about rental car insurance.

As I was on the phone with the customer service rep I took notes about all the things I needed to keep in mind about the Car Rental Loss & Damage program and these are the ones that stood out in my mind.

First off, the plan is only available if you use your American Express card to reserve and pay for the whole rental. The first few items are probably the most important, the rest are just nice to know.

1) Credit Card Insurance is Secondary Coverage – If you damage the car, American Express covers excess charges that aren’t covered by your auto insurance policy. For most people this means that they’ll pay your deductible. You send the declarations page of your insurance policy to American Express to show the amount of your deductible, you can submit a claim at yourcarrentalclaim.com

2) No Liability Coverage – The Loss & Damage Insurance Plan offers excess collision, comprehensive, and theft coverage. There is no liability coverage provided with your American Express Card. If you damage property other than the rental car or injure anyone, the insurance does not cover it.

3) CDW Invalidates Plan – The terms of the Loss & Damage plan require you to decline the car rental company’s Collision Damage Waiver and Theft Protection commonly referred to by rental car companies as CDW.

4) Other Drivers Allowed – As long as the additional drivers are listed on the rental agreement, those people are covered if they damage the car. The plan will pay the deductible on their auto insurance, if they don’t have insurance then they’ll pay up to your deductible.

5) Limited Time Offer – Coverage is provided for vehicles rented for 30 consecutive days or less. If you’re there for more than a month, don’t get into an accident on your 31st day.

6) Leprechaun Exclusion Clause – If you hit a Leprechaun the plan won’t cover any damage because Ireland is excluded in the plan terms. The insurance coverage applies in all but six countries around the world. There is no coverage provided for vehicles rented in Ireland, Australia, New Zealand, Italy, Israel and Jamaica.

7) Gas Guzzler Exclusion Clause – If you’re earning a ton of cashback on your gas credit card for the rental, chances are your vehicle may not be covered. Cargo Vans, Custom Vans, Pick-up Trucks and moving vans such as U-hauls aren’t covered.

8) Big SUV Exclusion Clause – Compact Sport Utility vehicles are covered, however, there is no coverage provided for full size sport utility vehicles such as a Ford Expedition.

9) $50,000 Cap – The coverage under the Rental Loss & Damage Insurance Plan only applies on cars worth under $50K. So if you rent a BMW 535i or a big fat Mercedes E350 and put a dent in it, don’t expect to have your deductible covered.

10) Extra Coverage Available – Okay, so it probably isn’t a surprise that there’s premium car rental protection available for a fee. It runs $24.95 for the period of the rental and it serves as your primary insurance on the car.

The main thing to remember when you’re dealing with insurance is to read all the terms and conditions so you know what’s covered.

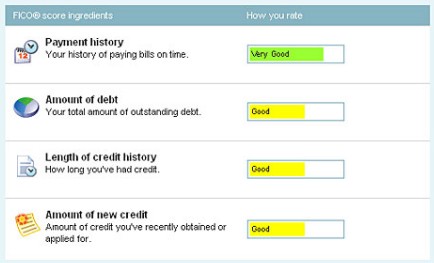

myFICO Review

myFICO is the consumer credit score site of the creator of the FICO credit score system, Fair Isaacs. You have several options on the myFICO site for finding your FICO score online and monitoring your FICO score. myFICO does charge for access to your score but offers a free credit score trial to let you check out their ScoreWatch service. You can also find occasional discounts via their myFICO promotions.

myFICO & Your Score

You probably already know that your FICO score is the credit score that many lenders — and even some insurance agents and employers — use to determine what sort of financial risk you represent. Variations of the FICO score are used in a number of ways to determine approval and rates for your mortgage, car loans, and credit cards. However, the FICO score is used by 90% of the largest banks and 100 of the top 100 U.S. credit card issuers so it’s the heavy hitter when it comes to credit scores.

myFICO Standard

At the most basic level you get your FICO score, plus receive an explanation about what it means and an idea of how lenders view you.

You can choose to see your FICO score from either TransUnion or Equifax, Experian no longer participates. FICO standard also includes a credit report from TransUnion or Equifax, whichever FICO score you choose – your score will likely vary somewhat across credit bureaus.

The FICO Standard score and report is $19.95, but as mentioned earlier you can see your credit score and credit report at no charge if you sign up for a free trial of ScoreWatch.

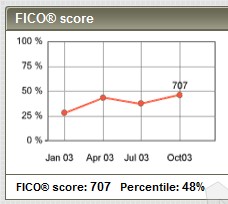

myFICO ScoreWatch

ScoreWatch allows you to get two FICO scores and two credit reports from Equifax each year, and it keeps tabs on changes to your credit score.

If you’re looking for the trending of your FICO score rather than just a snapshot then Scorewatch can be useful. For example, if you’re trying to improve your credit score and want to see progress, ScoreWatch gives you a graph of your score over time as well as regular updates:

- Monitors Equifax credit report daily & FICO score weekly

- Target credit score notifications

- Notifications when you qualify for a better interest rate

- FICO score drop alerts due to changes in your credit report

FICO Quarterly Monitoring

If you’re not actively tracking your credit score but want to check in on it a few times a year, FICO Quarterly monitoring can help you keep tabs on your score.

As you may know you’re able to get a free credit report every year from each credit bureau from annualcreditreport.com. This service uses TransUnion and makes your credit report and credit score available every quarter. The one extra credit report you get from the myFICO service is nice but you might not really feel like you need it. The main benefit of this service is that you get your credit score in addition to your credit report.

So every three months you receive a score and report, and an explanation of the positive and negative items affecting your score. You can identify problem accounts, as well as look for ways to improve your credit situation. The Quarterly Monitoring service will also alert you to changes in your credit score.

In the event that the change was due to identity theft, myFICO’s Quarterly Monitoring also provides identity theft insurance for up to $25,000 and a hotline to help you file id theft reports and complaints.

Suze Orman’s FICO Kit

While ScoreWatch and Quarterly Monitoring are setup to keep track of your credit score over time, the Suze Orman FICO kit is designed to walk you through the steps to help improve your credit. Created along with personal finance author Suze Orman, there’s more coaching and what-if analysis in the FICO kit.

Suze Orman’s FICO Kit gives you three credit reports and scores a year. The kit also includes the FICO Kit Action Planner that helps you take the information in your credit report and plan out steps to improve your score.

You can tailor the tool to your personal situation with their tools like the debt eliminator, bill pay reminders, and online coaching to help you get a car loan or home loan are included. You can also use the FICO Simulator, which allows you to estimate the effect certain changes would have your score.

You can use this myFICO promo code to get a discount on the FICO kit – SUZEFKP

2011 Federal Income Tax Brackets

Income Tax Brackets 2011

The 2011 tax brackets have been released by the IRS with the official tax rates that you’ll use when you pay your federal income tax next year. As you start looking for tax credits and deductions to lower your income taxes for the year that just ended you’ll use the 2010 federal tax brackets.

We originally published these as the projected 2011 tax rates back in 2010 but the federal tax cuts were extended last minute. Thanks to the extension of the Bush tax cuts the 2011 tax rates that the IRS released were more favorable for high income earners.

The projected 2011 income tax rates would have introduced another tax bracket at the higher end. The marginal tax rate for some in the 33% tax bracket would have dropped to 28% and for others would have risen to 36%. However, the projections didn’t become reality so the number of tax brackets remains the same in 2011.

Remember, the 2011 taxes coming out of your paycheck will be a little lower thanks to the payroll tax cut that applies this year only. Here are your 2011 income tax rates:

| Single Tax Bracket | Tax Rate | Tax Calculator |

|---|---|---|

| $0-$8,500 | 10% | |

| $8,500-$34,500 | 15% | |

| $34,500-$83,600 | 25% | Free Tax Calculator |

| $83,600-$174,400 | 28% | |

| $174,400-$379,150 | 33% | |

| $379,150+ | 35% |

| Married Filing Jointly Tax Bracket | Tax Rate | Tax Calculator |

|---|---|---|

| $0-$17,000 | 10% | |

| $17,000-$69,000 | 15% | |

| $69,000-$139,350 | 25% | Free Tax Calculator |

| $139,350-$212,300 | 28% | |

| $212,300-$379,150 | 33% | |

| $379,150+ | 35% |

| Head of Household Tax Bracket | Tax Rate | Tax Calculator |

|---|---|---|

| $0-$12,150 | 10% | |

| $12,150-$46,250 | 15% | |

| $46,250-$119,400 | 25% | Free Tax Calculator |

| $119,400-$193,350 | 28% | |

| $193,350-$379,150 | 33% | |

| $379,150+ | 35% |

It is worth noting that tax tables change each year. Most of the time, these changes are quite insignificant, reflecting small adjustments to where certain incomes fall. Brackets are are adjusted to reflect inflation.

You might not even notice from year to year. However, the small changes eventually add up, and you might be shocked one year to find out just how much things have shifted. If you are interested in making the most of your money, it is important to know your tax bracket, and to be aware of where you might fall so that you can get the tax deductions you need to increase your tax efficiency.

How is Your Income Taxed?

The good news is that all of your income is not taxed in one bracket. That would make it rather difficult for many — even those in the 15% or 25% bracket — to meet their tax obligation. Instead, your income is taxed in different brackets.

For example, if you make $150,000 a year, and your status is married filing jointly, you would presumably be in the 28% bracket. However, your entire income is not taxed in that bracket. The first $17,000 of your income would be taxed at 10%. From $17,000 – $69,000 would be taxed in the 15% bracket. Your income from $69,000-$139,350 would be taxed at 25%. Only the portion of your income that falls between $139,351 and $150,000 would actually be taxed at 28%.

Understanding Your Tax Status

Your tax bracket is determined in part by your tax status, so it is a good idea to know what different terms mean. Here is a quick look at how to determine your filing status:

- Single: Unmarried, filing individually.

- Married Filing Separately: Married, but filing individually. Remember that only one of you can claim the dependent exemptions.

- Married Filing Jointly: A married couple that files taxes together in a single return.

- Head of Household: Does not claim marital status, but has dependent exemptions to claim.

- Qualifying Widow/Widower: If your spouse died within the last two years, and if you are unmarried and have dependent exemptions to claim, you can use this status.

Tax Calculator 2011

If you’re wondering what the tax rates mean to your family, you can run the numbers with this free tax calculator.

Disclaimer: I am not a tax professional. The information here represents the best of my knowledge. Before making tax decisions, do your own research, or consult with a tax professional.

Why I Joined a Gang

It all started back in 2006 when I started chatting with a guy named Henry about personal finance and blogging. We became friends and started connecting with other people who were interested enough in personal finance to write about it every day online.

We were all going through similar things and got a lot out of sharing information with each other and going to one another for help. Eventually we decided we needed a “home base” where we could share our ideas and questions and decided to start our own “blogging gang” online – The Money Writers.

Of course, there was nothing nefarious about the gang, as the title might suggest. We were just a bunch of blogging buddies helping each other figure things out. I credit this group of people with helping me learn a tremendous amount about personal finance and the world of blogging. Without them, I don’t know that I would have been able to keep Money Smart Life running all these years.

Why You Should Join a Gang Too

The reason I’m telling you this is that building a support group can help you enormously in life. Having a trusted group of people you can go to for questions, help, or even just support can make the difference between success and dismal failure at whatever you’re doing.

Whether you’re trying to lose weight, manage your finances, be a stay-at-home parent, start a business, etc – having a support group help the process along and prevent you from feeling alone and overwhelmed.

There may already be groups of people that you could join up with. If not, you can always contact people you know that are in your same situation and start up your own. It helps if everyone brings something a little different to the table – different skill sets, personalities, perspectives, etc.

For example, here are the members of our group and their specialties. Of course everyone has multiple things they’re good at – here are some of their specialties and a recent article from their site.

Our Philosopher & Career Expert – Brip Blap

The Tax Expert – My Dollar Plan

The Canadian Branch – Million Dollar Journey

Our Frugal Expert – Frugal Dad

Retirement Expert – Generation X Finance

Life Hacks Expert – Lazy Man and Money

Our Deal Expert – Suns Financial Diary

Innovation Expert – The Digerati Life

If you’re struggling with a part of your life right now, think about joining (or starting) a group of people that can help you and one another press through to success.

Enter Your Email below to request free access to the member newsletter and article updates.

I'm Ben Edwards and I've been addicted to personal finance since I was 12 years old.

That passion for money has paid off for my family - so in 2006 I founded Money Smart Life to help you afford the life that you want. Read My Story...